Where did the magical drop in inflation go?

“Transitory inflation” proponents promised us disinflation for 18 months. I still see nothing.

Disclaimer: We live in a very uncertain time, and the world showed how unpredictable it has been in the past 2 years. Chances are that whatever one writes about this topic, he will -at best- be partially wrong. I decided to still take the risk.

This only reflects my thoughts, and it is not investment advice.

I wrote this article the week of the 14th February, before the situation in Russia escalated, and I didn’t change it. Obviously, it has a risk to worsen supply issues, but let’s leave this aside for a moment.

To understand the nature of inflation, it is important not to be drawn into technicalities. Technocrats, often proponents of the MMT (See post on modern monetary theory), will often try to trick you and confuse you with meaningless details.

What matters is to see the big picture and without external factors, the status quo should be your base case. To achieve that, here are 3 points I want to discuss today:

There are mathematical rules which define the appropriate level of interest rates.

Technical details are purely subjective, everyone will have pros & cons.

High prices drive higher prices. Low prices don’t drive lower prices.

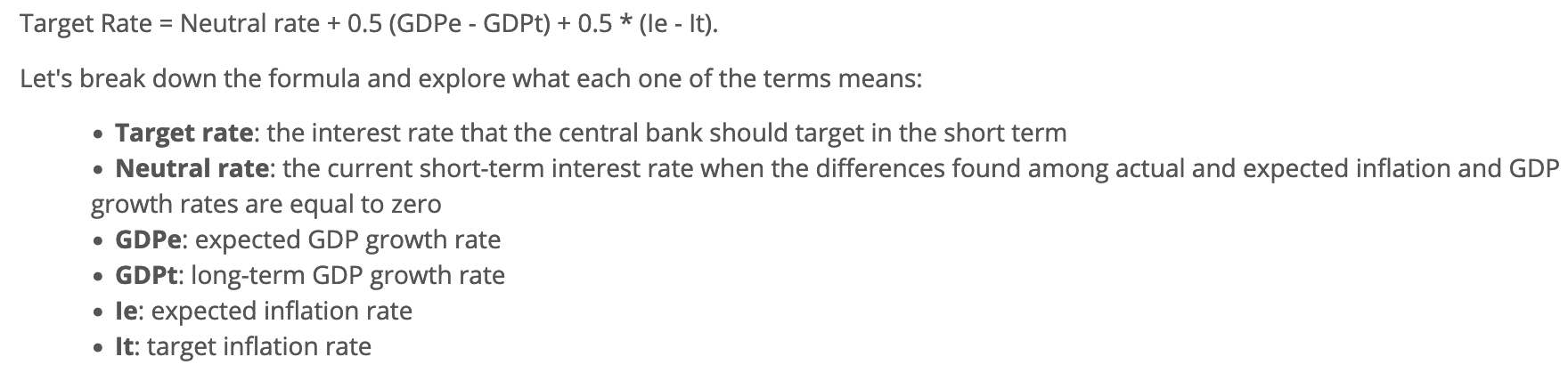

1. The Taylor Rule.

This rule computes the ideal interest rate in order to bring short term economic stability, while sustaining long-term expansion.

Central banks should increase short-term interest rates when one or both of the following occurs:

inflation rate exceeds the target inflation rate, OR

the anticipated GDP rate of growth exceeds its long-term rate of growth

Conversely, they should decrease interest rates if both of these happen:

inflation rates are below the target AND

GDP growth rates are below what was expected

Formula for the Taylor Rule

The fact is very simple: to bring inflation to 2%, the Fed needs to increase rates to 13%.

To bring inflation to 5%, which is more realistic in my opinion, the Fed Fund should be 12%. Only a couple of weeks ago, these were 9% & 7%. This is the problem of letting inflation run out of control.

The main issue is that the US is running above its potential output.

2. Central banks broke the rules, they justified this with fuzzy arguments.

There are mathematical formulas ruling the world. You have learned these when you were a kid. Would you every try to contradict them?

In this case, the mathematical formula says interest rates should be much higher. Of course, an external event can always happen suddenly reduce the American output, in which case we could go back to an equilibrium state.

Central banks & MMT advocates (model monetary theory, see previous newsletter) have justified breaking these rule with some kind of shaky arguments. Now they face an unprecedented situation with only bad options.

Back to the formulas.

1 + 1 = 2

Even if my local supermarket tells me 1 + 1 = 3?

Yes, in our mathematical system 1 + 1 = 2

End of the debate.

Anything else will be subjective arguments supporting your / their bias.

There will always be cases demonstrating that inflation can go lower or higher. For example, @wolfofwolfst demonstrates that shelter inflation will add 110 bps to the inflation rate in 2022 & 2023.

Earlier, in October, I explained why the rise in CPI wasn’t over.

Again, all of this is highly subjective & speculative, therefore, irrelevant.

3. Higher prices drive higher prices. Low prices don’t drive lower prices.

Going further, you need to refute the central argument for letting inflation run higher than necessary. Central Banks argue that lower prices mean that people will stop buying if prices fall.

This is illogical: will you delay the purchase of a car if yours broke down & that you need a new one to go to work? Recent history showed us people will still buy at any price. Will you stop buying food if food is getting more expensive? I hope you agree, this makes no sense.

This is mathematically incorrect. This assumes that if you buy a new car now, you don’t have any benefits to it. Let’s see it like this:

If you buy a car in year 1, you will get benefits (going to work, happiness, etc), and you will have the costs associated to this.

Your total value of the car will be these benefits reduced by the costs.

You expect this value to be positive, otherwise you wouldn’t buy the car.

Now if you buy it in 5 years, even at a lower price, you won’t have enjoyed that positive value in the first 5 years.

On the contrary, when people expect higher prices, they rush to buy & this is why central banks—normally—want to fight inflation

Conclusion

To conclude, I want to ask you this question: “What magical force will suddenly make inflation fall?”

This is what the “transitory inflation advocates” claim since 18 months now. I heard every argument and their contrary. Yet, it didn’t happen.

Of course, we won’t need to see 13% because as the Fed will increase rates, the economy will slow down and converge towards its potential. Much before we reach that level, we will see short term positive real yields and progressive default of the “zombie companies”, further reducing output and inflation. As of today, these companies that don’t generate enough profit to service their debt make up 10% of American companies.

If you want to know more about real rates, here is a previous article:

In addition, central banks are fighting a secular trend of physical & labor resources depletion.

If this sounds counterintuitive to you, I invite you to read this article of the IMF:

https://www.imf.org/external/pubs/ft/fandd/2016/03/juselius.htm

These two secular trends could drive inflation higher for a prolonged period. I will discuss that in a coming article. You can subscribe following this link: