The stock market is a giant Ponzi that Central Banks are trying to rescue at all costs

I will look at why Central Banks are putting so much effort to rescue markets.

First I want to look at who owns stocks. Households own the majority of stocks, but in reality, they’re also the ultimate owners of funds (pension, retirement, mutual) and ETFs.

As business holdings, HF, etc. make share is quite low, I will take the simplistic approach that only households are owning stocks.

There are 2 categories of stocks buyers: households & corporations ( buybacks). The formers are buying stocks for their price appreciation & dividend. They plan to make money out of it and sell when they need to ( e.g. during retirement). The latter are buying back stocks to improve their financial ratios and make the stock more appealing to investors.

So we know that investors (workers) are buying stocks when they have extra money, to use when they will need that money, for example during retirement.

If we look at the working-age population we can see that it is rolling over. It means that the amount of people contributing to the price appreciation of stocks is diminishing. At the same time, the share of the elderly is increasing.

Here’s how the age pyramid looks like for the #US.

Over time you may end up in a scenario like Japan.

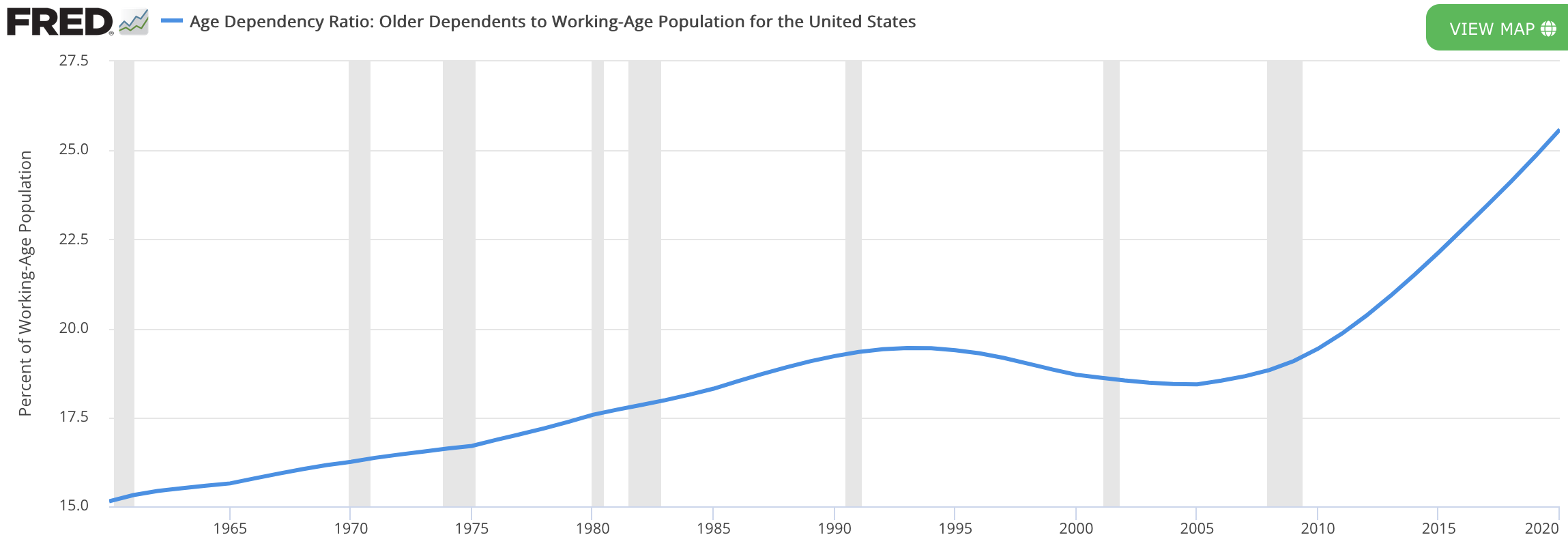

And this is why the so-called dependency ratio increases over time.

So if the dependency ratio increases, it means that relatively to before, the ratio of people buying to selling stocks are decreasing. Correct?

If the equilibrium is broken, stocks go down, but if they do, the newer working-age generations are not interested to invest and getting less money than what they put in, right?

Still, stocks go up. Or more or less…

Investors have good faith that the Central Banks will do their best to save the Ponzi, so they keep on investing.

CBs have developed different steps to make sure that stocks go “up only”:

Zero-interest rates

Quantitative Easing

QE with yield curve control

Outright purchases of ETFs (JP is already at this step)

The history of Japanese monetary policies.

As the number of retirees is increasing, the pressure is mounting to increase returns to be able to pay pensions. Again, fewer people contributing, more people benefiting. As you can see, funds are taking a risky bet to borrow to be able to meet redemptions. A sign of the trouble to come?

The population decline is something that never happened before. It is certain that if a negative spiral were to start in the stock markets it would be hard to inverse the momentum. I may also add that crypto offers new alternatives for the newer generation willing to avoid being sold out by their elderly.

Very interesting post. Brief and well presented. That 'sold out by the elderly' might ring true. Imagine, the ultimate Boomer kick in the ass on the way out. That said, the Boomer's kids will get much of those funds, if the Boomers don't spent it all.

Great post. Well thought out and presented. Wouldn't that be that last kick in the ass from us Boomers. That said the Boomer kids will get the money in the end, if there's anything left. That will drive wealth disparity though. Wealth will largely depend on the parents that you picked.