The myth of efficient markets

Part 1. What is the Efficient Market Hypothesis?

It is a hypothesis that states that share prices reflect all information and consistent alpha generation -aka beat the market on the long run- is impossible. Therefore, stocks always trade at their fair value, making it impossible for investors to purchase undervalued stocks or sell stocks at inflated prices.

According to that theory, because investors are rational and they have access to relevant information (public and private) prices reflect the true value of the underlying asset.

It also means that the price today is already an anticipation of the price at a distant future date discounted at an appropriated discount rate. It therefore concludes that market participants should correctly anticipate the future changes in policies & future discount rates.

If the price today is already the best price possible taking into account all information, why aren’t markets moving in a continuous fashion but rather will display wild swings from one day to another?

Part 2. Is the market efficient on the long term?

Here is a chart of the S&P using log scale for visibility, with MA100 months.

From this view, it seems the market has a clear upward movement, the market oscillating around this long term movement. Several factors can explain this like technological improvement or diminishing discount rates, this is not the topic so I won’t go more into details. This view is consistent with my previous posts on interest rates and increasing price to earnings, all having a strong long term movement.

Links to the posts:

P/E:

Real Rates:

We can visually see that there are two factors at play: a larger trend and a smaller trend that mean revert around the larger trend. It seems that on the long term, the market is efficiently capturing the information about discount rates, improving efficiency and increasing liquidities. From that perspective, it seems the best way to consistently generate returns is to consistently invest in the broad market.

Part 3. Historical examples

Index: Japan. 1980-1990.

What happened is that in the ‘80s the Japanese government engaged into a humongous credit impulse and devaluation of the Yen. Their planned economy succeeded for some time to provide greater economic output for companies in Japan, the world called “The Japanese economic miracle”. The wealth increase created a positive spiral that translated in greater market returns. Companies started to set up trading & real estate units as the profits from these units were greater than their regular business.The main idea was that free money would continue to flow in forever, until the music stopped.

For more, see the “Princes of the Yen”.

One need to explain to me: if the market was efficient and all information was priced in, how is it possible that investors didn’t foresee an inevitable change in policies?

Following this, the entire uptrend retraced. How come investors suddenly thought that their investments were actually worth 2/3 less than a few months before?

Individual stock: Enron 2001

If you are not familiar with the matter, you can read the article of the FT posted below.If markets were efficient, how could the markets omit publicly available information that Enron was a fraud? Why would markets still believe in sell-side analysts trying to unwind positions to the public?

Source: https://www.ft.com/content/80a6ee52-98ee-4ccc-8183-a68968c5fc9a

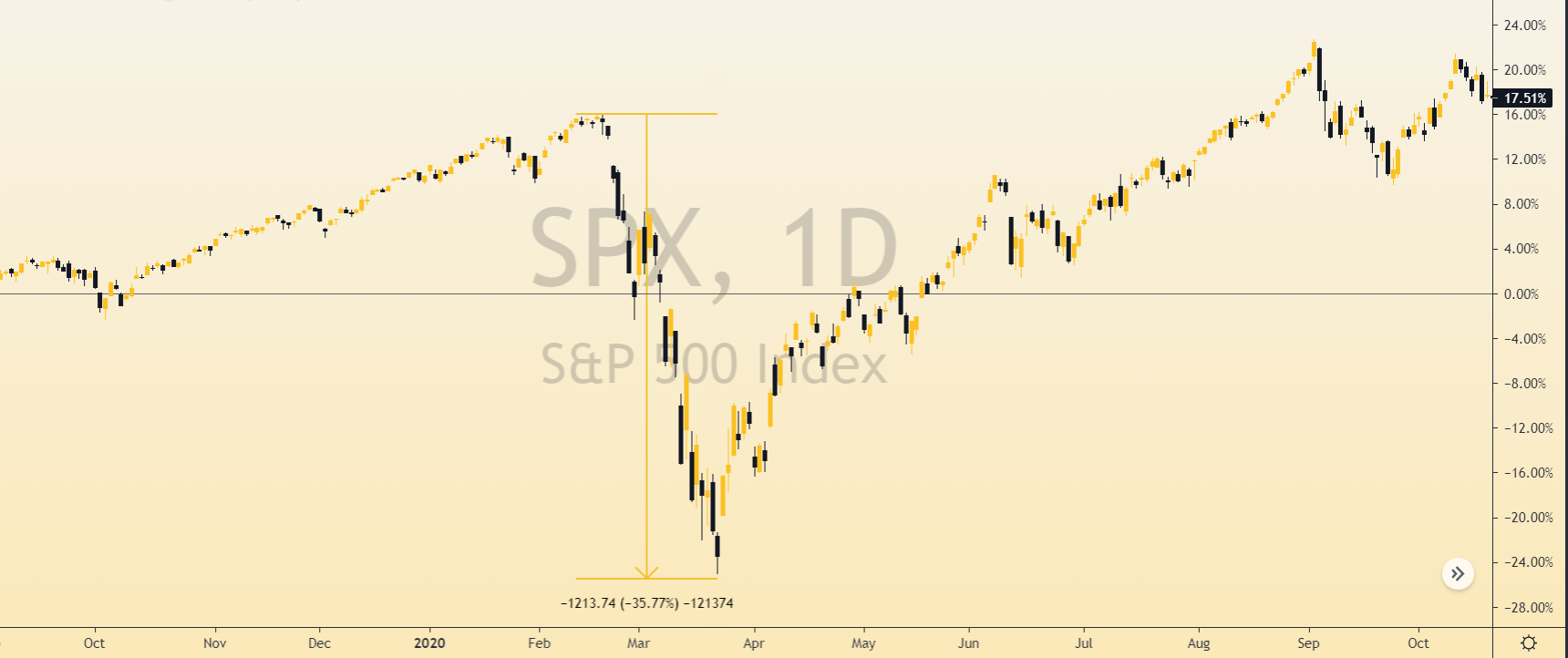

Last example, the S&P draw down of March 2020.

In 2020, 3 months after the global COVID pandemic started, the S&P suddenly dropped by 35%. How come markets failed to anticipate the FED’s & government’s stimulus response? Shouldn’t millions of brains and computers be able to anticipate that in an election year, every effort would have been made to pump the markets? So why did the S&P fall if the market participants could anticipate these things?

Part 4. Conclusions

On the long run, markets are seemingly efficient as they correctly pick up macro movements and revert to the mean when in excess or in deficiency. Stock picking and correct timing sound to be the prerogative of some highly skilled traders and investors such as W. Buffett. The reality appears to confirm the theory that it is practically impossible to consistently beat the market on the long term. However, at any given moment in time stocks and markets trade at a level that does not reflect their true value. Why do I say that?

Historical examples tend to show us that investors behave in an irrational manner (either irrational exuberance or irrational fear). Or to phrase it differently, most investors behave rationally most of the time but the remaining can have disproportionate impact on asset prices. These investors likely start in a rational manner but progressively lose touch with reality, first gradually then more and more quickly, getting stuck in a recency bias and failing to understand that markets don’t move uniquely in one direction.

Asset prices never really move in a linear manner but rather in wild swings, which contradicts the theory of having all information priced in at all time. In my view, only black swan events could trigger these large swings as they are the only “sudden new information events”.

The theory is self contradictory, as it states that it’s impossible to generate consistent alfa. It however relies on investors’ knowledge who try to beat the market…

Low liquidity in some markets at some moment in time seems to be exacerbating price movement (such as for alt-crypto currencies).

Why is this happening?

Markets are a momentum animal, the crowd moving all together in one direction like a herd of sheep, amplifying their greed, confidence or fear. A rational mind trying to make sense would easily be confused by such a behavior and theoreticians had to put some imaginary tales like the “invisible hand”, a God-like phenomenon, to explain market movements.

How can investors avoid being trapped in their emotions?

Very few individuals or firms in the world are able to successfully beat the market in the long run and I would recommend any random Joe to read and follow Ben Graham principle to investing.

Part 5. Bonus.

One could think that with the recent increase in individual investors should bring a superior level of information in the markets as it should, in theory, bring more information to the markets. But I think this cyclical generation of late stage investors rather destroys information quality by bringing sub-par knowledge into the pool of market information. For example, let’s look at when these retail flows into an ETF like $ARRK. It appears that their timing has been incredibly wrong since good third of them bought right at the top.

Another example is the death of short sellers. Many view them as the devil of the markets, but I see them as a necessary part of it, bringing a balance through advance research, like the Ying & the Yang of the markets. The recent attacks of Masa Son or Billy Huang (taking cover with the Redditors of WSB on hedge funds like Citron Research or Melvin Capital) are an example that the crowd is not brining additional knowledge but rather killing essential market equilibrium actors. Billy boy finally fell and others will follow.

Nice didnt read all. But ill save this to continue during the week!!

Great article bro.. - Pirate