Central Bank Digital Currencies

a primer

From Oct. 20 to Jan 21, the ECB ran a public consultation on CBDC - Central Bank Digital Currencies - there were 8K respondents (out of 342M inhabitants or 632K @ECB Twitter followers). It is needless to say that they tried to keep it as discreet as possible.

“Privacy” emerged as the key feature that CBDC should have, followed by “Security”. Are these the main concerns that the population should have? For example, security is a core feature of blockchain technologies, so why even mention it? As for the rest of the propositions, I will let you judge them and evaluate later what are the real concerns.

Part 1. What are CBDCs?

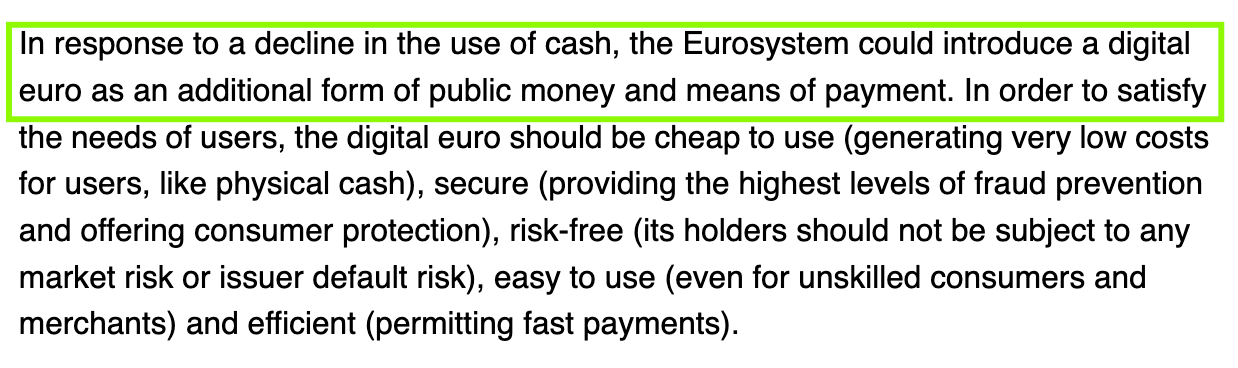

It is a digital form of currency that is backed by a CB (Central Bank) and has legal tender status (see notes for more details).

This means it is recognized by law as a power of discharge for a debt, that the creditor cannot refuse that cash to settle the debt, and that the monetary value is equal to the amount indicated on the mean of payment. Currently, notes and coins are considered legal tender, electronic money such as the one you have on your bank account is not legal tender but is usually accepted to settle a debt. In summary, it is a banknote but digital. Replacing cash could thus be one of the main objectives of CBDCs.

CBDCs are using DLT (Distributed Ledger Technology), a “distributed and redundant storage of data across thousands of nodes”. Blockchain (used for cryptocurrencies such as Bitcoin) is a specific type of DLT, the difference being that cryptos are using decentralized ledgers while CBDCs would use private ledgers (maintained by the CBs).

Part 2. How did we get there?

After using barter, humans developed the first monetary systems in the form of coins. During the Middle Ages, gold was replaced by paper gold, a promise of exchange for real gold coins. Then came the book paper (a physical ledger), in a nutshell, your bank balance which was later digitalized (your bank accounts, a digital ledger). In this evolution from real to digital, CBDCs come as the natural next step.

Part 3. How will CBDCs work?

CBDCs eliminate the need for banks to hold your money. CBs would verify directly the transactions between the parties without transiting through your bank. The bank business will be narrowed down to the services: trading, wealth management, advice.

Here are some schematics that explain the changes.

Part 4. Why are CBs so keen to move forwards on CBDCs?

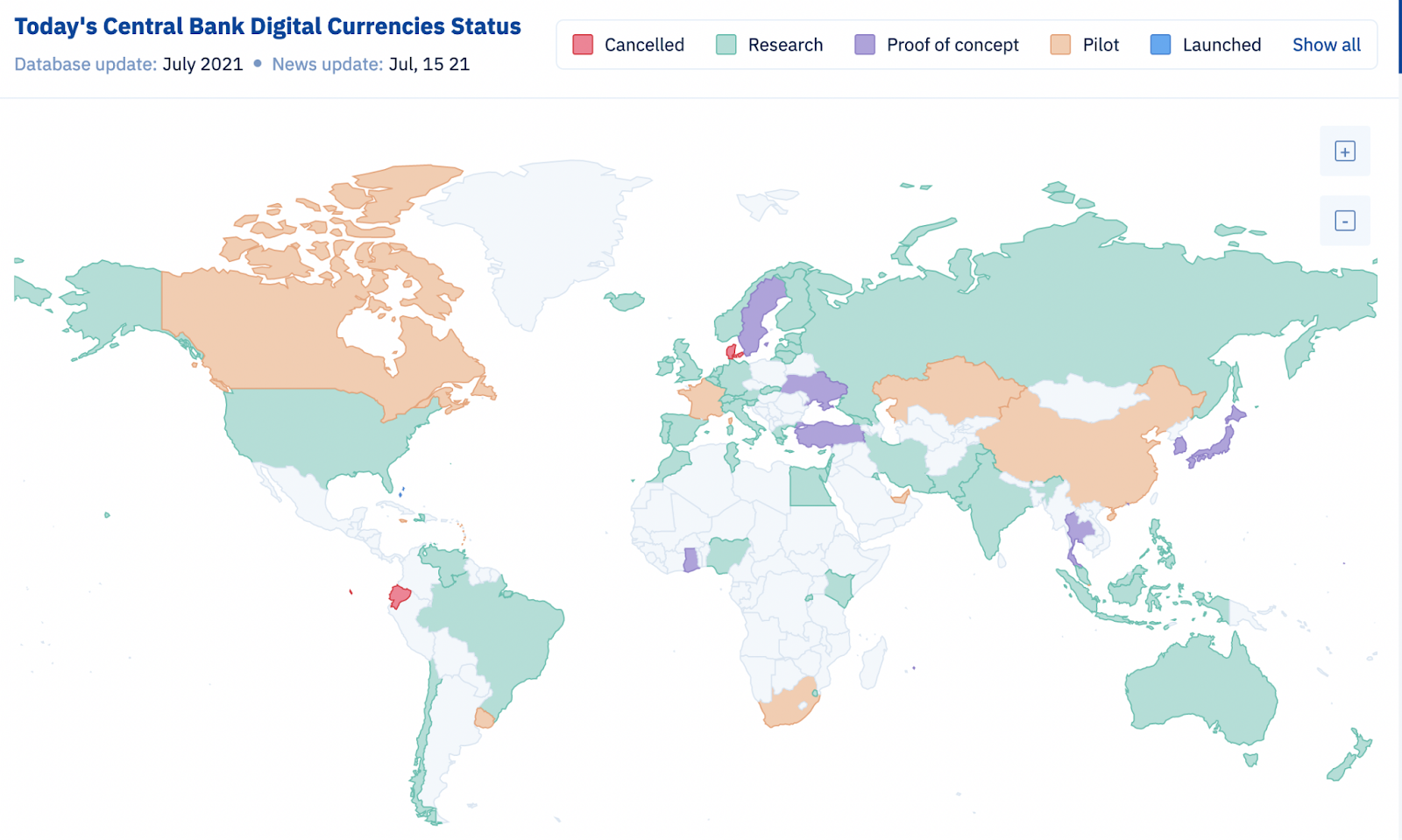

Most CBs are planning to launch them and some are already piloting solutions (CN, FR CA). Chinese soft launch happened last year when they gave away free CBDC for the Lunar New Year.

Remove physical cash

It offers

More control on money laundering and fraud

Fewer technical issues or booking errors

Faster speed, lower costs & more security (vs. notes & coins)

Fight stablecoins

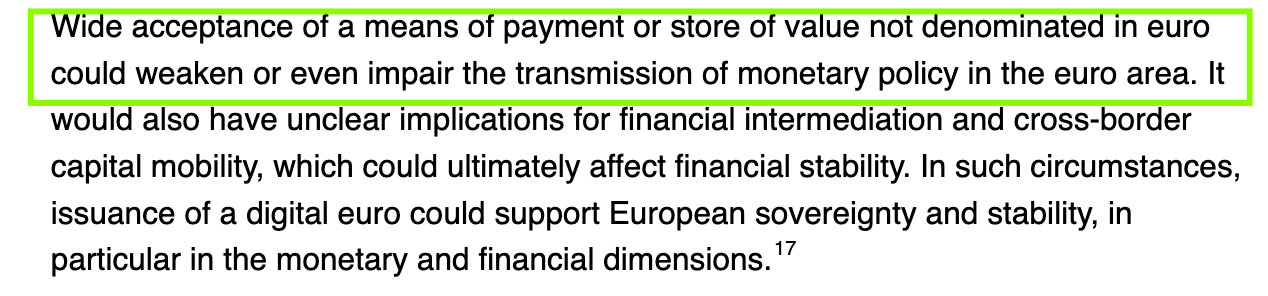

There is an acknowledgement from the ECB that cryptocurrencies & stablecoins adoption could impair the ECB ability to conduct its monetary policies. Most people are aware of the questions surrounding Tether and its unregulated “money printing”.

ECB public consultation report

New tools to implement monetary policy

This is probably the main reason for CBDCs implementation, if you remember my post on real yields, you know that these are irremediably going into the negative territory. CBs will thus need to change how they operate.

Central Banks were established to deal with monetary disarray (US) or hyperinflation (FR) and are not equipped with tools to deal with subdued inflation and growth. Their tools include reserve requirements, discount rate, (open) market operations. I let you refer to the post on QE which explains why QE has little to no impact on growth, jobs or inflation.

CBDCs will bring new options to the CBs toolkit. In the US the FED cannot “print money” as it falls into the scope of the US Treasury, so they would gain that ability. In Europe, the ECB is entitled to do so with National CBs acting as agents but they are limited on how they can use that “money”.

CBDCs would therefore enable them to “print money” and allocate it at their best convenience (central banks or central planners?). When doing QE, they could for example decide to lend money to certain industries (Japan is trying this for the moment). They could also send helicopter money to the population to encourage spending and spur inflation.

Control the population spendings

Another important reason.

Because of the CBs immediate reach into users' digital wallets, they could decide how people spend their money. To encourage spending, they could put an end date to the value of money, for example by decreasing the value of money in your wallet as time goes by-as this was the case during the Chinese pilot-. They could also force the allocation of unspent amounts to specific investments (for example, to negative-yielding government bonds). They could prevent overweight people from eating in fast-foods, people & companies to maintain a maximum carbon footprint and the list goes on as they have unlimited options.

Give more freedoms to banks

As banks wouldn’t hold money CBs could give them more freedom like removing reserve requirements as they wouldn’t hold customers money. They would just be a normal company that you don’t need to bail out every 10 years.

Conclusions:

While CBDCs are undoubtedly the path forward of money by making the current payment system faster, more secure and cheaper. However, the advantages for the individual or corporate end-user in technologically advanced economies would be limited. For example, Europe had SEPA for a while, this offers instant free cross-border transactions and a change to e-EUR wouldn’t provide many benefits for the population.

On the other hand, it comes with big warning signs in terms of -financial- freedom. It will be critical to keeping the population and the companies informed on CBDCs development. CBs will need more transparency to make sure the population can safely accept this new means of payment.

Notes.

Note 1. Diagram of the current monetary system (US)

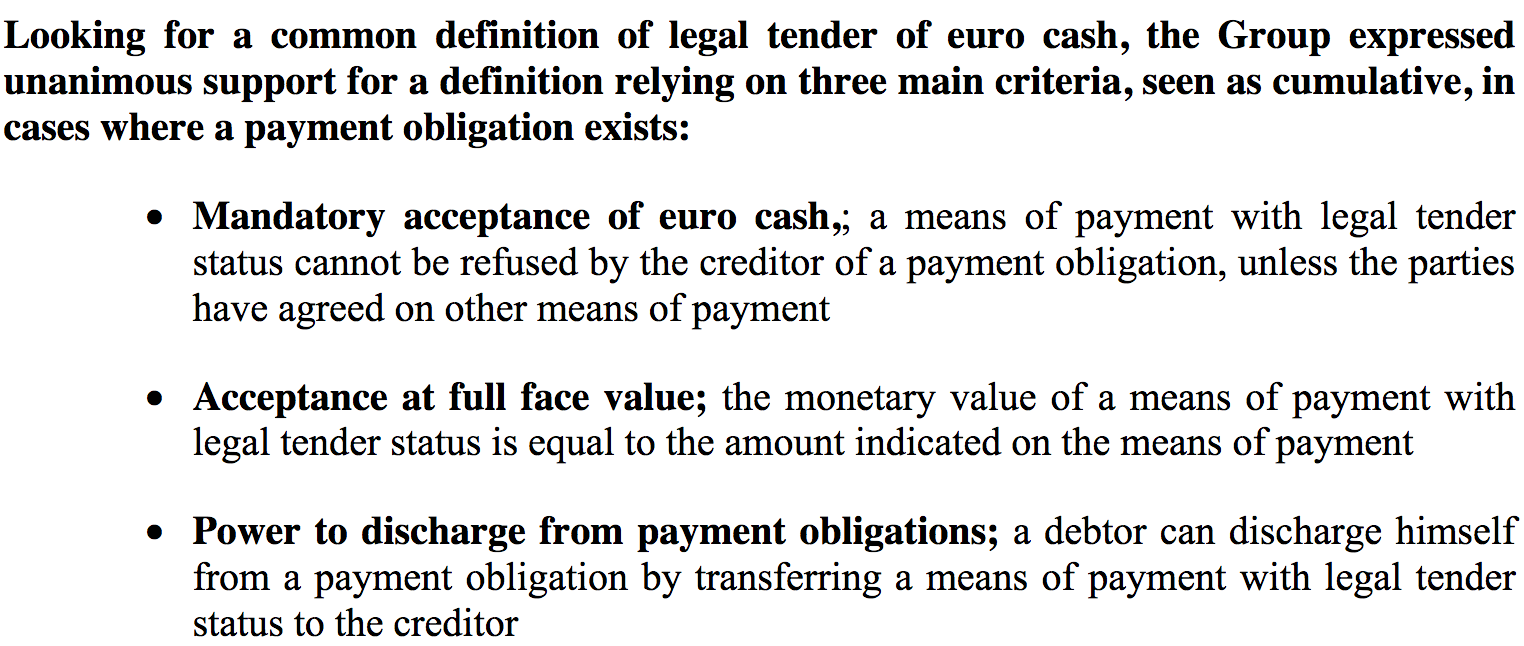

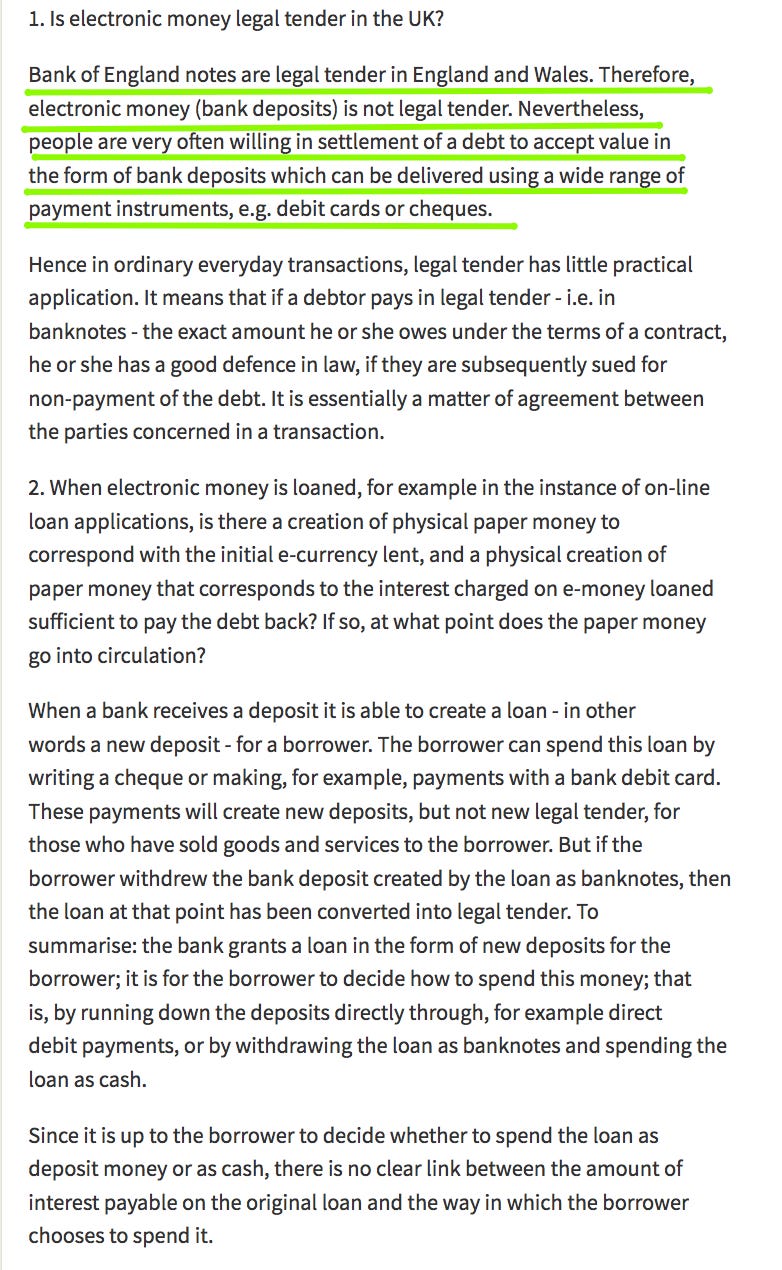

Note 2. What is “ legal tender”? Definitions from the ECB & BoE.

ECB

Electronic money such as the one you have on your bank account is not legal tender but is usually accepted to settle a debt.

https://ec.europa.eu/economy_finance/articles/euro/documents/elteg_en.pdf

BoE

Note 3. Summary of the public consultation

Sources

https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf

https://www.marketreview.com/how-banks-operate/

https://forkast.news/digital-dollar-project-foundation-white-paper-cbdc/

https://www.suerf.org/policynotes/12575/overview-of-central-bank-digital-currency-state-of-play

https://morethandigital.info/en/central-bank-digital-currency-cbdc-digital-money-for-our-central-banks/